In a dramatic move to tackle its escalating housing affordability crisis, the Australian government has unleashed a colossal £1.2 billion (A$2.3 billion) initiative designed to catapult first-time buyers onto the property ladder. The expanded Home Guarantee Scheme is set to revolutionise the market by slashing the required deposit to a mere 2% for thousands of eligible applicants.

The scheme, a cornerstone of the recent federal budget, represents one of the most aggressive interventions in the housing market in recent years. It aims to assist a staggering 50,000 Australians annually, including single parents and key workers, by having the government act as a guarantor for the bulk of the loan.

Who Qualifies for the Property Lifeline?

The initiative is structured into three distinct streams, each targeting a specific demographic struggling with housing affordability:

- First Home Guarantee: 35,000 places for first-time buyers seeking to construct or purchase a newly built home with just a 5% deposit.

- Regional First Home Buyer Guarantee: 10,000 places exclusively for individuals or families purchasing in regional areas, also with a 5% deposit.

- Family Home Guarantee: 5,000 places dedicated to single parents with dependent children, allowing them to buy a home with an astonishingly low 2% deposit.

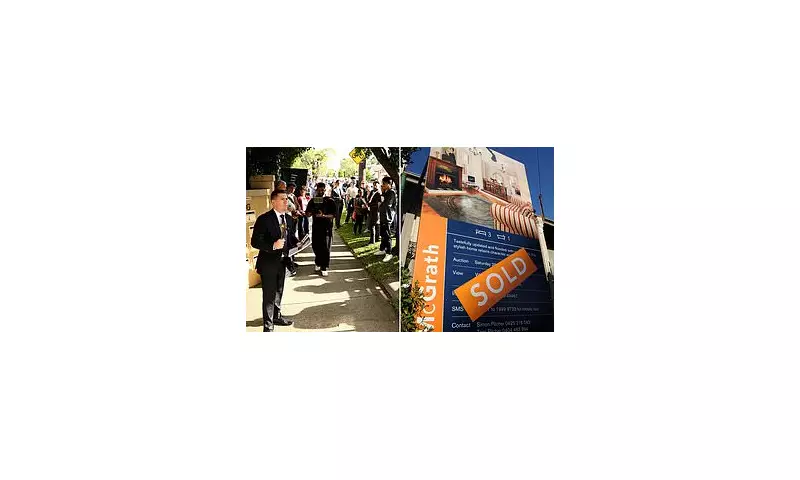

The Stark Reality of Australia's Housing Market

This radical policy comes against a backdrop of a fiercely competitive property market. Data reveals a daunting landscape for aspiring homeowners, with the national median dwelling price soaring to approximately £480,000 (A$912,000). In major metropolitan hubs like Sydney, the figures are even more eye-watering, with median prices often exceeding £850,000 (A$1.6 million).

The scheme effectively eliminates the need for costly Lenders' Mortgage Insurance (LMI), a significant barrier for many saving for a traditional 20% deposit. This could save buyers tens of thousands of pounds upfront.

A Heated Debate: Solution or Time Bomb?

While hailed by the government as a vital lifeline, the policy has ignited a fiery debate among economists and property experts. Proponents argue it provides crucial assistance to 'mortgage prisoners'—those who can comfortably service a mortgage but are trapped by the inability to save a large deposit amidst rising rents and living costs.

However, sceptics voice grave concerns. They warn that injecting such a large number of highly leveraged buyers into an already supply-constrained market could inadvertently pour petrol on the fire of house price inflation. The core risk, they argue, is that while access to ownership improves in the short term, overall affordability could worsen for everyone if prices are driven higher.

The success of the scheme now hinges on a delicate balance: can it empower new buyers without overheating the market? All eyes will be on Australian property data in the coming months to see if this bold gamble pays off.