Inflation in the United Kingdom has remained stubbornly at 3 per cent for the past month, official data revealed today, a figure that was recorded even before the outbreak of conflict in the Middle East began to impact global markets.

Inflation Persists Above Target

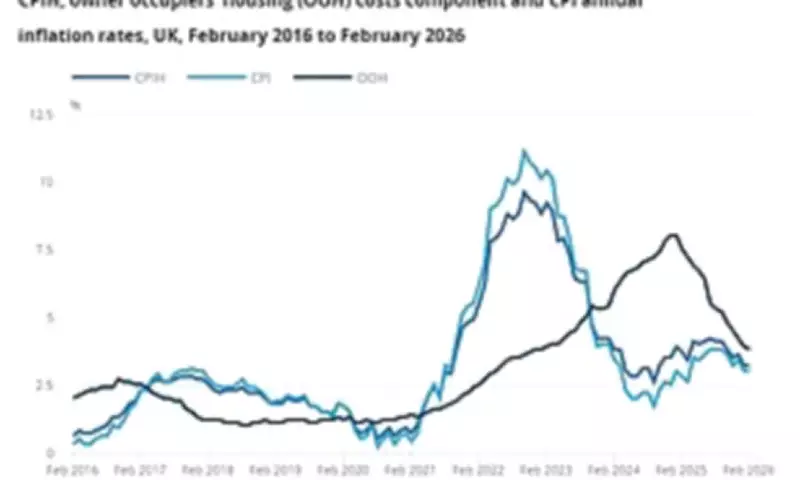

The headline Consumer Price Index (CPI) rate matched market expectations, yet it continues to sit significantly above the Bank of England's 2 per cent target. This persistence dashes earlier hopes that price rises might be on a steady downward trajectory, with economists now revising their forecasts in light of recent geopolitical turmoil.

Middle East Conflict Clouds Economic Outlook

The chaos triggered by US-Israeli attacks on Iran has severely muddied the economic outlook. Economists have been forced to rip up previous projections, warning that the war could lead to sustained inflationary pressures. The Bank of England stated on Thursday that recent increases in wholesale energy costs, partly driven by the conflict, will delay the return of CPI inflation to its target.

Rachel Reeves, commenting on the situation, said: 'In an uncertain world we have the right economic plan, taking a responsive and responsible approach to supporting working people in the national interest.' She outlined government measures, including taking £150 off energy bills, providing targeted support for heating oil costs, protecting consumers from unfair price rises, reducing food prices, and cutting red tape to enhance long-term energy security.

Revised Forecasts and Economic Volatility

The Bank of England now expects inflation to hover around 3% in the second quarter of 2026, a sharp increase from the 2.1% forecast in February. Central bankers emphasised the volatile nature of the current situation, noting that events over the next six weeks could clarify the scale of disruption and its impact on prices.

Economists have weighed in with their own projections. Mr. Allenby, for instance, now anticipates CPI inflation exceeding 4% during the second half of 2026. He explained: 'Under our updated assumptions, we now anticipate a much sharper rise in petrol prices, while higher wholesale gas prices cause a 19% increase in the Ofgem energy price cap in July.'

Pantheon Macroeconomics echoed this sentiment, agreeing that if the recent spike in gas prices is sustained, CPI could head towards 4% later this year. This outlook underscores the broader economic uncertainty, with fuel and energy costs being key drivers of inflationary pressures.

Broader Implications for the UK Economy

The sustained inflation rate, compounded by geopolitical tensions, poses significant challenges for policymakers and consumers alike. Higher energy and fuel prices are likely to filter through to other sectors, potentially stifling economic growth and increasing the cost of living. The government's response, as outlined by Reeves, aims to mitigate these effects, but the volatile global environment adds a layer of complexity to long-term planning.

As the situation evolves, all eyes will be on upcoming data and geopolitical developments to gauge whether inflation can be tamed or if further spikes are on the horizon, reshaping the UK's economic landscape for years to come.